How Much Can I Borrow For Student Loans

How Much Can I Borrow for Student Loans?

The amount of money you can borrow for student loans depends on a number of factors. Your family’s income, the cost of your school and your academic performance are among these factors.

Costs

The cost of attending college is a major factor that determines how much you can borrow for student loans. The federal government has set an annual limit on what it will pay for tuition, room and board, and other expenses at different types of schools. These limits are called “cost of attendance” (COA) allowances. For example, if you’re attending a public university, your COA allowance will be higher than if you attend a private university with similar costs and academic offerings.

Your family situation may also affect how much you can borrow. If your parents make less than $50,000 per year combined, they may qualify for additional aid by completing the Free Application for Federal Student Aid (FAFSA). Eligibility for assistance from the federal government is based on both income and assets; families with more assets may be required to pay back more in loans after graduation than those who have fewer assets available to them when calculating repayment amounts later down the road (or at all).

How Much Can I Borrow For Student Loans

Student loans aren’t limitless. The maximum amount you can borrow depends on factors including whether they’re federal or private loans and your year in school.

Undergraduates can borrow up to $12,500 annually and $57,500 total in federal student loans. Graduate students can borrow up to $20,500 annually and $138,500 total.

» MORE: Your guide to financial aid

But just because you can borrow that much doesn’t mean you should. To keep higher education affordable, calculate how much you should borrow for college based on your expected future earnings and aim to keep your student borrowing below that amount.

Federal student loan limits

The maximum you can borrow depends on your year in school, your status as a dependent or independent student, and the type of loan. There are three main types of federal student loans: Direct subsidized, direct unsubsidized and direct PLUS.

To apply for federal student loans, submit the Free Application for Federal Student Aid — this FAFSA guide walks you through the process.

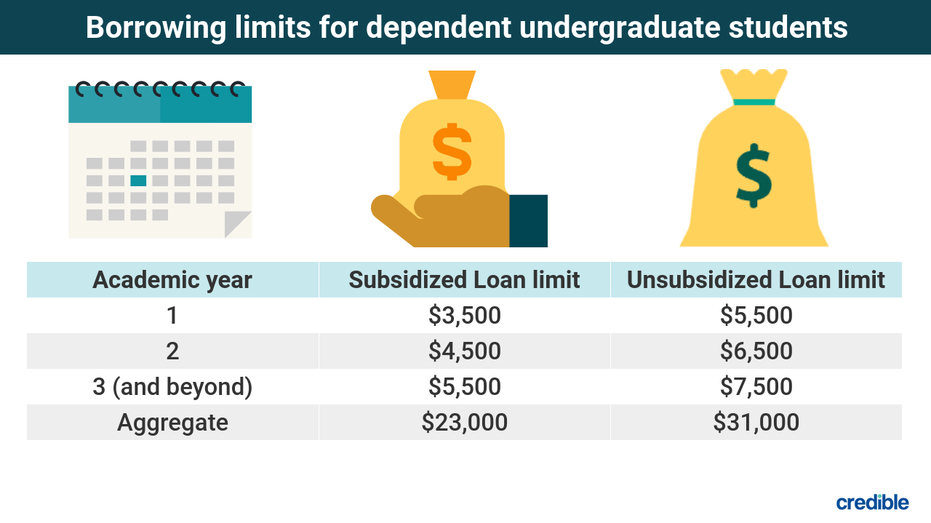

The amount of money you can borrow in federal student loans depends on your student status. If you are an undergraduate, the maximum amount of Direct Subsidized and Direct Unsubsidized Loans you can borrow each academic year is between $5,500 and $12,500, depending on your year in school and your dependency status (whether you are a dependent or independent student). A parent can also borrow a Direct PLUS Loan to help pay for the educational costs of a dependent undergraduate student. If you are a graduate/professional student, the maximum amount you can borrow each academic year is $20,500 in Direct Unsubsidized Loans. A graduate/professional student is also eligible to borrow a Direct PLUS Loan. The maximum Direct PLUS Loan amount that a parent or graduate/professional student may borrow is the cost of attendance, minus other financial aid received.

student loan calculator

Make extra payments to pay off student loans faster. If you can free up more money for payments right now, you can cut down the total interest you pay, too.

Use this student loan payoff calculator to determine your debt-free date, then see how much time and money you could save by making extra student loan payments. You can see an amortization schedule as well.

| Average National Student Debt$28,400 | Total Monthly Payment$297 |

If you refinance your loans at a 3.66% rate then your loan payments will be $163 lower a year. See Refinance Rates

| LOAN | LOAN AMOUNT | INTEREST RATE | LOAN TERM | MONTHLY PREPAYMENT | MONTHLY PAYMENT | |

| Loan 1 | years | $297 | ||||

College is supposed to be fun, right? Hollywood sure thinks so: in movies like Old School, Legally Blonde and Accepted, it’s one-half wild parties, one-half intellectual and emotional discovery. But that’s Hollywood—the schools themselves paint a different, but equally attractive picture. Open any admissions office pamphlet and you’ll find students lounging cheerfully in grassy campus spaces; friendly, approachable professors chatting with small clusters of adoring undergrads; clean, peaceful dormitories; and constantly perfect weather.

While both of these portrayals contain some truth (there are parties; the weather is nice sometimes), there’s one aspect of college that is often left out, or at least pushed to the sidelines: the price tag. While it’s no secret that getting a degree has grown more expensive in recent years, the numbers are nonetheless surprising. The cost of tuition and fees at public four year institutions increased by 17% over the past five years alone, according to data from The College Board.

Before using the student loan calculator above, come prepared with a few pieces of information about your loan.

Loan amount

Loan amounts vary depending on whether you’re exploring a federal or private student loan. The loan amount you’re offered might also be limited based on your enrollment level (e.g., undergraduate versus graduate or professional student) or degree program.

Federal student loan amounts

Undergraduate students:

- Direct Subsidized Loans: Up to $5,500 annually.

- Direct Unsubsidized Loans: Up to $12,500 annually.

Graduate students:

- Direct Unsubsidized Loans: Up to $20,500 annually.

- Direct PLUS Loans: Up to the school’s reported cost of attendance, minus other financial aid received.

Parents of dependent undergraduate students:

- Parent PLUS loans: Up to the school’s reported cost of attendance, minus other financial aid received.

Private student loan amounts

Loan amounts for private student loans can vary by lender. Each lender sets its own borrowing criteria, annual borrowing limits, interest rates and repayment terms. In general, private student loan lenders offer loan amounts that cover the gap between a school’s cost of attendance and any other financial aid a student receives. Some lenders also impose lifetime borrowing limits, which may be up to $150,000 or more for some degrees. Regardless of whether you borrow federal or private student loans, borrow only the amount you need per school year after exhausting all grant and scholarship options. If you must take out loans to finance educational gaps, consider maximizing federal student loan limits before turning to a private student loan, as federal student loans come with additional benefits like income-driven repayment plans and standardized hardship programs.

Loan term

Your loan term is the amount of time you have to repay the loan in full. For federal student loans under a standard repayment plan, the default loan term is 10 years. However, student loans that are under an alternative payment plan offer terms from 10 to 25 years. Like private student loan amounts, private student loan repayment terms vary by lender. Terms for private student loans can be as short as five years and as long as 20 years. A shorter loan term can help you save more money on interest charges during your repayment period but result in a larger monthly payment. Some lenders offer lower interest rates as an incentive for a short term length. On the flip side, a longer term for your student loans will lower your monthly payment but will accumulate more interest charges over time. Before borrowing student loans, make sure you know all of the term options your lender offers so you can choose the right path for your financial needs.

Interest rate

The interest rate you’re offered depends on the type of lender you’re pursuing and your financial picture. Federal student loans offer the same interest rate to all borrowers, regardless of credit score or income. Private student loans, on the other hand, will often do a credit check and set interest rates according to your creditworthiness. The higher your credit score, the lower your interest rates. Keep in mind that the lowest interest rates advertised on lender websites may not be available to you. To find out what interest rates you’ll receive, take advantage of lenders’ prequalification features, if available. Prequalification allows you to input basic details about yourself and your desired loan in exchange for a snapshot of the rates and terms offered.

For many students, the only way to stay atop this rising tide has been by taking on an increasing amount of student loans. The result has been skyrocketing student loan debt over the past decade.

Not so fun, that – but don’t get discouraged. Sure, some recent graduates have student loan horror-stories to tell: high debt, low job prospects and a load of other expenses to boot; and others have simply stopped bothering to make loan payments at all (the total number of people with defaulted student loans recently climbed to over 7 million). Many graduates, however, find their debt to be manageable, and, in the long run, worthwhile.

The important thing is to know in advance what you’re getting yourself into. By looking at a student loan calculator, you can compare the costs of going to different schools. Variables like your marital status, age and how long you will be attending (likely four years if you are entering as a freshman, two years if you are transferring as a junior, etc.) go into the equation. Then with some financial information like how much you (or your family) will be able to contribute each year and what scholarships or gifts you’ve already secured, the student loan payment calculator can tell you what amount of debt you can expect to take on and what your costs will be after you graduate – both on a monthly basis and over the lifetime of your loans. Of course how much you will pay will also depend on what kind of loans you choose to take out.

average student loan interest rate

The average student loan interest rate is 5.8% among all households with student debt, according to a 2017 report by New America, a nonprofit, nonpartisan think tank. That includes both federal and private student loans — about 90% of all student debt is federal.

With a 5.8% interest rate on $30,000 of student loans, a borrower would pay about $9,600 in interest throughout 10 years.

The average student loan interest rate is higher among some groups, according to the report. For instance, the average rate is 6.3% among households where the borrower didn’t complete a college degree, and 6.6% among households with incomes less than $24,000.

If you have multiple student loans with different rates, the weighted average interest rate is the rate you’ll have if you consolidate the loans through the federal government. Federal consolidation won’t lower your average interest rate, but refinancing with a private lender could.

If you have begun repayment of your federal student loans, their interest rates have been set to 0% until after Aug. 31, 2022, and no payment is due before then.

If you are still borrowing for your education, the federal student loan interest rate for undergraduates is 3.73% for the 2021-22 school year. Federal rates for unsubsidized graduate student loans and parent loans are higher — 5.28% and 6.28%, respectively. The rates for the coming year go into effect on July 1.

Private student loan interest rates can sometimes be lower than federal rates, but approval for the lowest rates requires excellent credit. If you have good credit, you may be able to refinance existing student loans to get a lower rate.

Current student loan interest rates

| Refinance student loans | |

| Fixed | 2.59% to 9.15% |

| Variable | 1.88% to 8.9% |

| Private student loans | |

| Fixed | 3.34% to 14.99% |

| Variable | 1.04% to 11.99% |

| Federal student loans (fixed) | |

| Undergraduate | 3.73% |

| Graduate | 5.28% |

| PLUS (Parent, Grad) | 6.28% |

Rates updated monthly.

Federal student loan interest rates are increasing for the 2021-22 school year and apply to loans disbursed between July 1, 2021, and July 1, 2022. The interest rates for all new federal direct undergraduate student loans are 3.73%, up from 2.75% in 2020-21. Unsubsidized direct graduate student loan rates are 5.28%, up from 4.30%. Rates for PLUS loans, which are for graduate students and parents, are 6.28%, up from 5.30%.Federal student loan interest rates by year

Federal student loan interest rates by year

To apply for federal student loans, as well as grants and work-study, fill out the Free Application for Federal Student Aid — this FAFSA guide can help. Any student, regardless of their financial need, typically qualifies for unsubsidized student loans, and students with a financial need may qualify for subsidized loans. Subsidized loans are a better deal because the government pays the interest that accrues while you’re in school.

Federal student loan fees are taken as a percentage of the total loan amount and deducted proportionally from each loan disbursement, meaning you’ll receive slightly less than the amount you borrow.

| Academic year | Undergraduate | Graduate | Parent PLUS, Grad PLUS |

|---|---|---|---|

| 2021-22 | 3.73% interest 1.06% fee | 5.28% interest 1.06% fee | 6.28% interest 4.23% fee |

| 2020-21 | 2.75% interest 1.06% fee | 4.30% interest 1.06% fee | 5.30% interest 4.24% fee |

| 2019-20 | 4.53% interest 1.06% fee | 6.08% interest 1.06% fee | 7.08% interest 4.24% fee |

| 2018-19 | 5.05% interest 1.06% fee | 6.60% interest 1.06% fee | 7.60% interest 4.25% fee |

| 2017-18 | 4.45% interest 1.07% fee | 6.00% interest 1.07% fee | 7.00% interest 4.26% fee |

| 2016-17 | 3.76% interest 1.07% fee | 5.31% interest 1.07% fee | 6.31% interest 4.28% fee |

| 2015-16 | 4.29% interest 1.07% fee | 5.84% interest 1.07% fee | 6.84% interest 4.27% fee |

| 2014-15 | 4.66% interest 1.07% fee | 6.21% interest 1.07% fee | 7.21% interest 4.29% fee |

Source: U.S. Department of Education, Federal Student AidInterest rates effective July 1 of each year. Loan fees effective October 1 of each year.

Private student loan interest rates by lender

It’s generally best to max out your federal student loan options before taking out a private student loan. If you need one, shop around first to ensure you get the lowest rate you qualify for. If you don’t meet a lender’s credit requirements, you can apply with a co-signer who does.

Current private student loan interest rates, updated monthly:

| Lender | Fixed APR ranges* | Get started |

|---|---|---|

| Fixed: 3.34% – 14.51% | CHECK RATES | |

| Fixed: 3.49% – 12.99% | CHECK RATES | |

| Fixed: 3.24% – 12.78% | CHECK RATES | |

| Fixed: 3.75% – 12.85% | CHECK RATES | |

| Fixed: 3.47% – 11.16% | CHECK RATES | |