Student loan repayment is a challenging and frustrating process. It can be hard to know where to begin, and even harder to stay on track.

Here are some tips for making the process of paying off student loans easier:

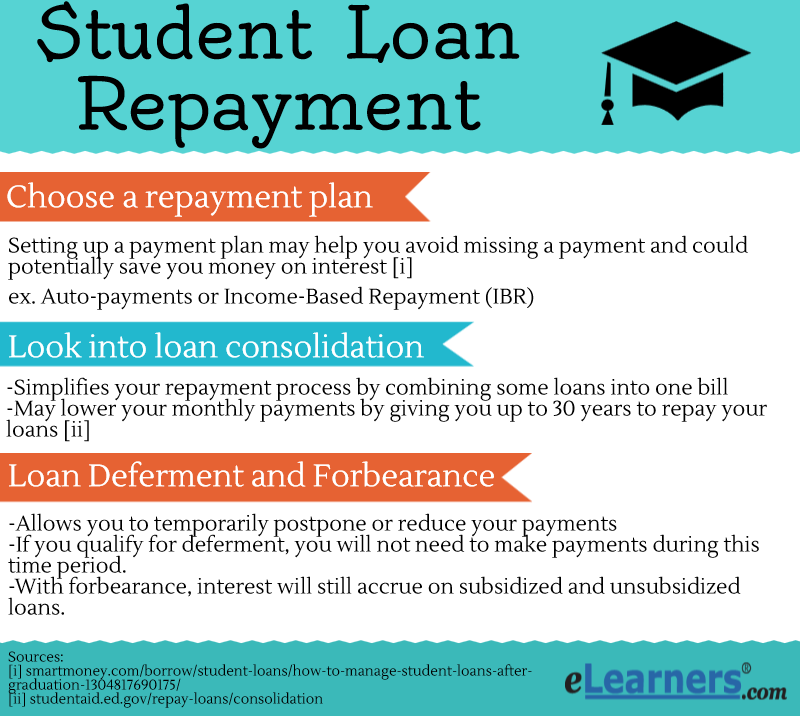

- Make a budget and stick with it

- Make extra payments every month

- Pay attention to fees and interest rates

- Keep track of your progress

Help With Student Loans Repayment

However, there are very specific eligibility requirements you must meet to qualify for loan forgiveness or receive help with repayment. Loan forgiveness means you don’t have to pay back some or all of your loan.

You never know what you may be eligible for, so take a look at the options we have listed below.

- Teacher Loan Forgiveness

If you teach full-time for five complete and consecutive academic years in certain elementary or secondary schools or educational service agencies that serve low-income families, and meet other qualifications, you may be eligible for forgiveness of up to a combined total of $17,500 on eligible federal student loans. Get the details about Teacher Loan Forgiveness here.

- Public Service Loan Forgiveness (PSLF)

If you work full-time for a government or not-for-profit organization, you may qualify for forgiveness of the entire remaining balance of your Direct Loans after you’ve made 120 qualifying payments—that is, 10 years of payments. To benefit from PSLF, you should repay your federal student loans under an income-driven repayment plan. Learn more about PSLF now! If you’re interested in PSLF, contact FedLoan, the PSLF servicer, as soon as possible at 1-855-265-4038.

If you have been denied loan forgiveness under PSLF because one or all of the payments you made on your Direct Loans were under a nonqualifying repayment plan, you might be eligible for Temporary Expanded Public Service Loan Forgiveness (TEPSLF). Learn more about TEPSLF and how to apply for this first come, first served opportunity.

- Income-Driven Repayment (IDR) Plan

If you repay your loans under a repayment plan based on your income, any remaining balance on your student loans will be forgiven after you make a certain number of payments over a certain period of time. Learn more about IDR plans and how to apply.

- Military Service

In acknowledgment of your service to our country, there are special benefits and repayment options for your student loans available from the U.S. Department of Education and the U.S. Department of Defense. Benefits include interest rate caps under the Servicemembers Civil Relief Act and Department of Defense student loan repayment programs. Learn more about federal student loan benefits for members of the U.S. armed forces.

- AmeriCorps

The Segal AmeriCorps Education Award is a benefit received by participants who complete a term of national service in an approved AmeriCorps program—AmeriCorps VISTA, AmeriCorps NCCC, or AmeriCorps State and National. After you successfully complete your service, you are eligible to receive a Segal AmeriCorps Education Award, which can be used to repay qualified student loans.

- Other Options

Check out the “Student Loan Forgiveness” page for information about other types of loan forgiveness and discharge that might be available if you meet certain conditions.

If the options listed above don’t apply to you, but you need help making your federal student loan payments, contact your loan servicer about the option to

donors that pay off student loans

About 45 million people carry student loan debt in the United States — to the tune of more than $1.7 trillion. The average student debtor graduates with $39,400 in student loans.

With that in mind, it’s no surprise that many people are trying to figure out how to get rid of this debt. Interestingly, there are donors that pay off student loans, as well as charities that help with student loans. Here’s what you need to know about getting donations to help with student loans.

Charities That Help Pay Off Student Loans

If you’re looking for charities that help with student loans, there are a few that can be good choices. Some might have requirements, such as volunteer work, in order to qualify.

Here are some of the charities that help with student loans.

Rolling Jubilee

Rolling Jubilee is a project of the Debt Collective, which focuses on debt abolition. It’s not just student loan debt, but all types of debt. As part of the effort, Rolling Jubilee buys the debt, for pennies on the dollar. Then, instead of making the debtor make payments, they just forgive the debt.

Shared Harvest Fund

Shared Harvest is an organization that offers student loan funds in exchange for volunteer work. You’re paired with charities and other nonprofits and as you volunteer, Shared Harvest puts money toward your student loan repayment. As a result of COVID-19 pandemic, there has been a shift toward those that can help in hard-hit communities. This can be an opportunity for student loan forgiveness for nurses.

Organizations That Offer Student Loan Repayment Assistance

Some of the organizations that provide loan repayment assistance include those that offer government-backed relief.

AmeriCorps

Rather than being a charity, AmeriCorps offers partial loan repayment after you complete 12 months of service. You need to work full-time and, on top of offering partial loan repayment, your time in AmeriCorps can be used toward qualifying for Public Service Loan Forgiveness (PSLF).

National Health Service Corps

There are various loan repayment assistance programs through the National Health Service Corps. Your level of loan repayment depends on your healthcare specialty and whether you work full-time or part-time. You also have to work in an area that is considered underserved. This can be one way to get student loan forgiveness for doctors.

Teach For America

For teachers willing to work in a low-income and needed area for at least five years, it’s possible to get up to $17,500 in loan repayment assistance. This is one option for student loan forgiveness for teachers.

Peace Corps

Peace Corps is another government-backed program aimed at volunteer work around the world. After you complete your service, you can receive partial loan repayment assistance. On top of that, this is another opportunity to work in a way that qualifies you for PSLF.

Donors That Help Repay Student Loans

For borrowers who aren’t eligible for loan forgiveness and repayment assistance through the above charities and government organizations, here are a few other channels to consider:

Crowdfunding

Another option is to get individual donations from people to help you pay off your student loans. Crowdfunding is a way to get small amounts of money from a lot of people to help pay down your student debt. Some of the popular crowdfunding sites include:

- LoanGifting

- GoFundMe

- YouCaring

Before you use crowdfunding, realize that it requires a lot of work to promote your campaign and raise money. Additionally, many crowdfunding websites take a cut, so you won’t necessarily get the full amount.

student loan forgiveness

In certain situations, you can have your federal student loans forgiven, canceled, or discharged. Learn more about the types of forgiveness and whether you qualify due to your job or other circumstances.

Types of Forgiveness, Cancellation, and Discharge

The summaries below offer a quick view of the types of forgiveness, cancellation, and discharge available for the different types of federal student loans.

The PSLF Program forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying employer.

PSLF Resources

- Public Service Loan Forgiveness (PSLF) Help Tool

- Public Service Loan Forgiveness (PSLF) & Temporary Expanded PSLF (TEPSLF) Certification & Application

- Limited PSLF Waiver Information

- Public Service Loan Forgiveness Program FAQ

- Submit a Public Service Loan Forgiveness Reconsideration Request

Qualifying for PSLF

To qualify for PSLF, you must

- be employed by a U.S. federal, state, local, or tribal government or not-for-profit organization (federal service includes U.S. military service);

- work full-time for that agency or organization;

- have Direct Loans (or consolidate other federal student loans into a Direct Loan);

- repay your loans under an income-driven repayment plan*; and

- make 120 qualifying payments.

To ensure you’re on the right track, you should submit a Public Service Loan Forgiveness (PSLF) & Temporary Expanded PSLF (TEPSLF) Certification & Application (PSLF Form) annually or when you change employers. We’ll use the information you provide on the form to let you know if you are making qualifying PSLF payments. This will help you determine if you’re on the right track as early as possible.

*This provision will be waived through October 31, 2022 as part of the limited PSLF waiver.

Suspended Payments Count Toward PSLF and TEPSLF During the COVID-19 Administrative Forbearance

If you have a Direct Loan and work full-time for a qualifying employer during the payment suspension (administrative forbearance), then you will receive credit toward PSLF or TEPSLF for the period of suspension as though you made on-time monthly payments in the correct amount while on a qualifying repayment plan.

To see these qualifying payments reflected in your account, you must submit a PSLF form certifying your employment for the same period of time as the suspension. Your count of qualifying payments toward PSLF is officially updated only when you update your employment certifications.

Digital signatures from you or your employer must be hand-drawn (from a signature pad, mouse, finger, or by taking a picture of a signature drawn on a piece of paper that you then scan and embed on the signature line of the PSLF form) to be accepted. Typed signatures, even if made to mimic a hand-drawn signature, or security certificate-based signatures are not accepted.

Note: In-grace, in-school, and certain deferment, forbearance, and bankruptcy statuses are not eligible for credit toward PSLF.

Have questions? Find out what loans qualify and get additional information about student loan flexibilities due to the COVID-19 emergency.

Qualifying Employer

Qualifying employment for the PSLF Program isn’t about the specific job that you do for your employer. Instead, it’s about who your employer is. Employment with the following types of organizations qualifies for PSLF:

- Government organizations at any level (U.S. federal, state, local, or tribal) – this includes the U.S. military

- Not-for-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code

Serving as a full-time AmeriCorps or Peace Corps volunteer also counts as qualifying employment for the PSLF Program.

The following types of employers don’t qualify for PSLF:

- Labor unions

- Partisan political organizations

- For-profit organizations, including for-profit government contractors

Contractors: You must be directly employed by a qualifying employer for your employment to count toward PSLF. If you’re employed by an organization that is doing work under a contract with a qualifying employer, it is your employer’s status—not the status of the organization that your employer has a contract with—that determines whether your employment qualifies for PSLF. For example, if you’re employed by a for-profit contractor that is doing work for a qualifying employer, your employment does not count toward PSLF.

Other types of not-for-profit organizations: If you work for a not-for-profit organization that is not tax-exempt under Section 501(c)(3) of the Internal Revenue Code, it can still be considered a qualifying employer if it provides certain types of qualifying public services.

Full-time Employment

For PSLF, you’re generally considered to work full-time if you meet your employer’s definition of full-time or work at least 30 hours per week, whichever is greater.

If you are employed in more than one qualifying part-time job at the same time, you will be considered full-time if you work a combined average of at least 30 hours per week with your employers.

If you are employed by a not-for-profit organization, time spent on religious instruction, worship services, or any form of proselytizing as a part of your job responsibilities may be counted toward meeting the full-time employment requirement.

Eligible Loans

Any loan received under the William D. Ford Federal Direct Loan (Direct Loan) Program qualifies for PSLF.

Loans from these federal student loan programs don’t qualify for PSLF: the Federal Family Education Loan (FFEL) Program and the Federal Perkins Loan (Perkins Loan) Program. However, they may become eligible if you consolidate them into a Direct Consolidation Loan.

Student loans from private lenders do not qualify for PSLF.

Under normal PSLF Program rules, if you consolidate your loans, only qualifying payments that you make on the new Direct Consolidation Loan can be counted toward the 120 payments required for PSLF. Any payments you made on the loans before you consolidated them don’t count. However, if you consolidate these loans into a Direct Loan before October 31, 2022, you may be able to receive qualifying credit for payments made on those loans through the limited PSLF waiver.

Qualifying Payments

A qualifying monthly payment is a payment that you make

- after Oct. 1, 2007;

- under a qualifying repayment plan;

- for the full amount due as shown on your bill;

- no later than 15 days after your due date; and

- while you are employed full-time by a qualifying employer.

Most of the PSLF qualifying payment rules have been suspended through October 31, 2022. Under this temporary waiver, you may get credit for payments you’ve made on loans that would not normally qualify for PSLF. These payments will count even if you didn’t pay the full amount or on-time. However, only payments made after Oct. 1, 2007 can count as qualifying payments. For more information, visit the limited PSLF waiver page.

You can make qualifying monthly payments only during periods when you’re required to make a payment. Therefore, you can’t make a qualifying monthly payment while your loans are in

- an in-school status,

- the grace period,

- a deferment, or

- a forbearance.

If you want to make qualifying payments, but you’re in a deferment or forbearance, contact your federal student loan servicer to waive the deferment or forbearance. However, you can still receive credit toward PSLF during the COVID-19 payment pause.

Your 120 qualifying monthly payments don’t need to be consecutive. For example, if you have a period of employment with a nonqualifying employer, you will not lose credit for prior qualifying payments you made.

The best way to ensure that you are making on-time, complete payments is to sign up for automatic debit with your loan servicer.